When to start taking CPP

“When should I start taking CPP?” is a common topic of discussion among Canadians approaching retirement. However, it is important to remember that retirement planning is not one-size-fits-all; the strategy that works for your friends or neighbors may not be the right choice for your specific financial situation.

How CPP Works

Canada Pension Plan (CPP) benefits are calculated based on several factors, which is why most people do not receive the maximum benefit at age 65.

To qualify for the maximum CPP, you generally need at least 39 years of maximum contributions between the ages of 18 and 65. In reality, many individuals fall short of this due to time spent in school, career gaps, periods of lower income, or early retirement.

Your CPP benefit at age 65 is directly tied to your personal contribution history. You can review this through your “Statement of Contributions,” available from the Canada Revenue Agency (CRA). This statement provides a detailed record of your earnings and contributions from age 18 and is a useful tool for estimating your future CPP income.

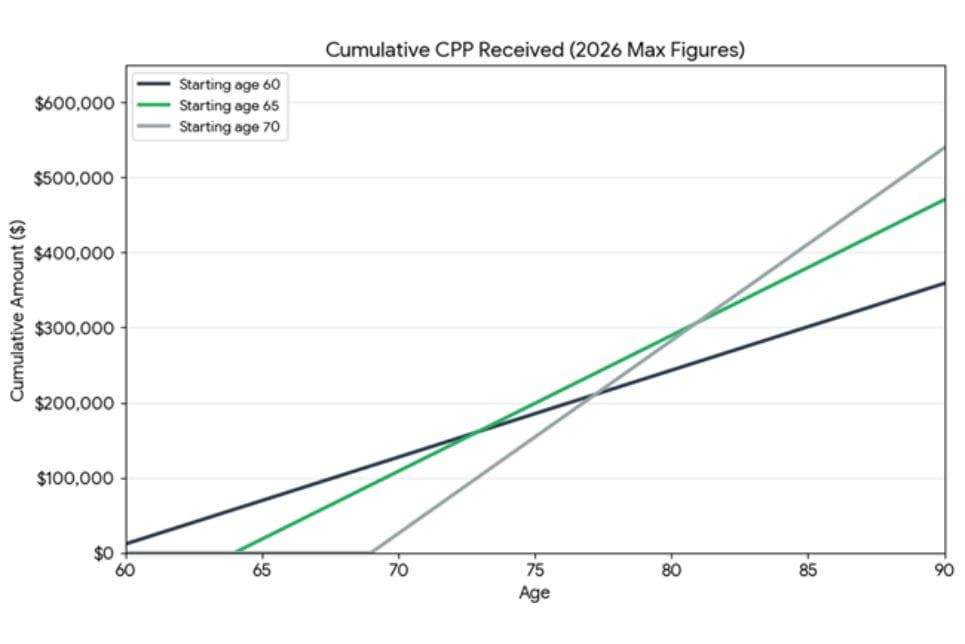

Breakeven Age

The decision of when to start taking your CPP may come down to your “breakeven age,” which is simply the point where delaying your pension results in a higher total amount received over time.

- CPP Start Age

- Age 60

- Estimated Breakeven Age

- Age 74

- What This Means

- Beginning CPP at age 60 provides income sooner and increases short-term cashflow. However, by age 74, the total amount received would generally be lower than if CPP had started at age 65.

- Age 65

- Baseline

- Starting at age 65 is considered the baseline, where your benefit is neither reduced nor increased.

- Age 70

- Age 82

- Delaying CPP until age 70 results in higher monthly payments. However, you would generally need to live beyond age 82 for the larger payments to outweigh the five years of deferred benefits.

CPP breakeven is calculated by comparing the total lifetime income from starting CPP at different ages. You estimate how much you receive per year at each starting age (adjusted for the reduction or increase factor), then project those payments forward over time and sum them up.

The breakeven point is simply the age where the cumulative total from two starting strategies becomes equal, for example, when “start at 60” catches up to “start at 65,” or when “start at 70” catches up to “start at 65.” After that age, the higher monthly option pays more overall.

Finances

Your current finances may be one of the most important factors to consider. If you are retiring and will rely on CPP income to cover your cost of living (food, shelter, and clothing) or to repay debt, then it likely makes sense to start collecting CPP as soon as it becomes available at age 60.

If you have other sources of income such as a company pension, RSP savings to draw on, or rental income, you will have more flexibility when to start collecting CPP.

Taxes

When managing multiple revenue streams, it is vital to evaluate the tax implications of your CPP timing. Because CPP is treated as taxable income, payments are subject to your marginal tax rate.

To optimize your retirement, we recommend collaborating with your Financial Planner and accountant to synchronize your CPP start date with other income sources. This strategic coordination ensures your distributions are structured to minimize your effective tax rate throughout your retirement years. Furthermore, a well-timed start can help manage your total net income to avoid the OAS Recovery Tax (clawback), protecting more of your Old Age Security benefits.

Summary

Deciding when to start your CPP is a personal choice that must weigh your immediate financial needs against your long-term goals. Because this choice permanently sets your monthly income, it is a cornerstone of any successful retirement strategy.

As you approach this milestone, we recommend reviewing your unique situation within a comprehensive financial plan. Please reach out to us to discuss how we can tailor a strategy to help you achieve the retirement you’ve worked for.

Disclaimers and Disclosures

CPP benefits are determined by Service Canada based on individual contribution history and program rules, which may change over time. The analysis presented is based on assumptions and estimates and should not be relied upon as a guarantee of future CPP entitlements or outcomes. For more information about the program, please visit: https://www.canada.ca/en/services/benefits/publicpensions/cpp.html.